The mortgage tax deduction is one of the most significant incentives available when purchasing property in Japan. It reduces the burden of income and resident taxes if the requirements are met.

1. Basic mechanism

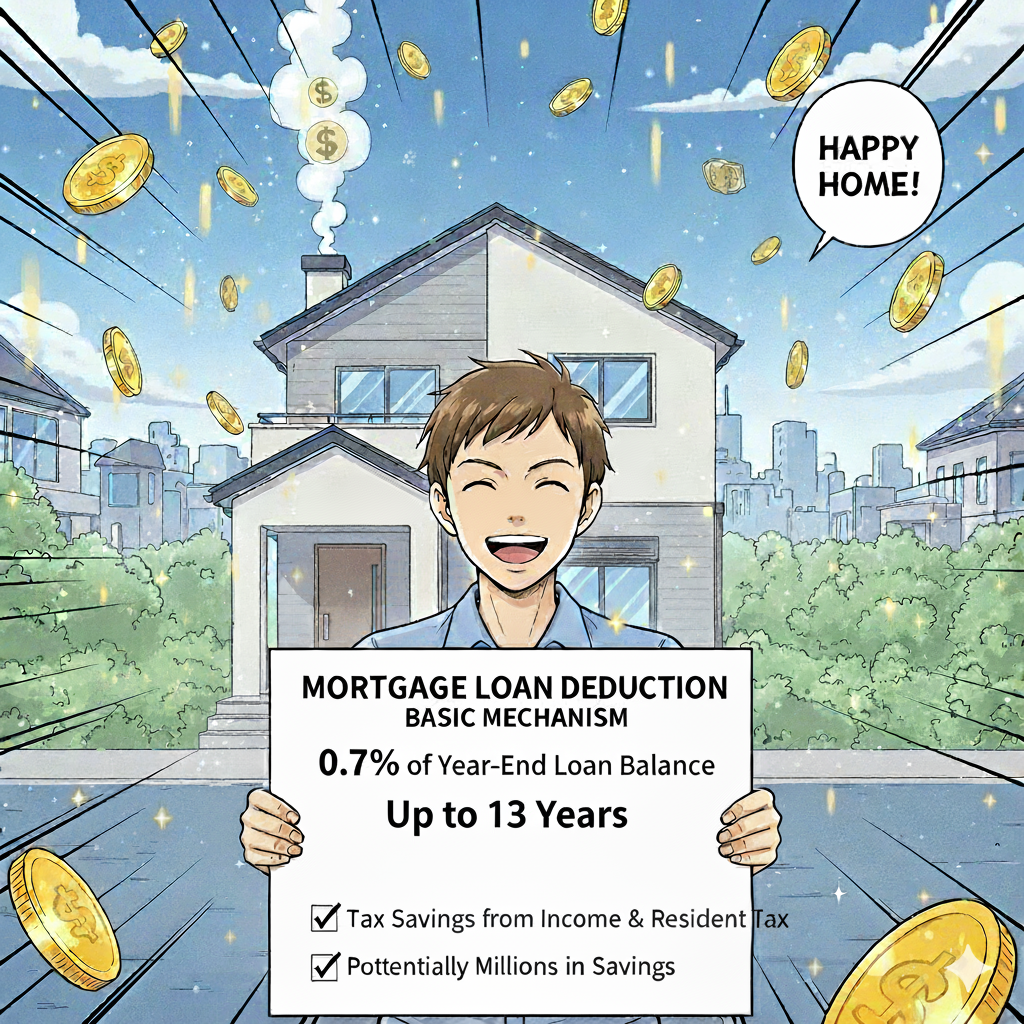

The deduction equals 0.7% of the year-end loan balance, available for up to 13 years.

Example: if the balance is ¥30,000,000, the first-year deduction is ¥210,000.

2. Key eligibility requirements

Floor area of 50㎡ or more

Move-in within 6 months of acquisition

Loan repayment period of 10 years or longer

Total annual income of ¥20,000,000 or less

3. Practical notes and case

Example: for a new house valued at ¥40,000,000 with a loan balance of ¥35,000,000, the first-year deduction is ¥245,000. Over 13 years, the total expected tax saving is ¥3,185,000.

Any deduction exceeding income tax can be applied against resident tax, but the cap is ¥136,500.

Takeaway

The mortgage tax deduction can generate savings in the millions of yen over time. Ensuring eligibility conditions are met and preparing the necessary documents in advance helps secure these benefits and stabilize financial planning.