1. Why consumption tax matters

Many investors assume residential rent is tax exempt, but short term rental income is treated differently. Accommodation fees are generally taxable, and as revenue grows the impact of consumption tax becomes material. Misunderstanding this point can distort expected cash flow.

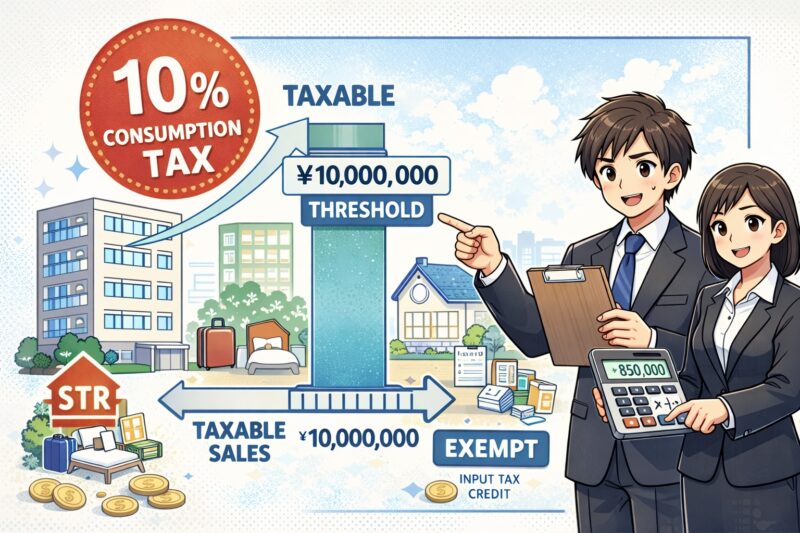

2. Defining taxable sales

Consumption tax liability is determined by taxable sales volume. In principle, if taxable sales in the base period exceed ¥10,000,000, the operator becomes a taxable business. STR accommodation fees count as taxable sales, while long term residential rent does not. This distinction is critical.

3. Numerical example

Assume annual STR revenue of ¥8,000,000 and long term residential rent of ¥6,000,000. Total income is ¥14,000,000, but taxable sales are only ¥8,000,000. In this case, the operator remains tax exempt. If STR revenue rises to ¥10,500,000, the business is likely to become taxable from the following periods.

4. Impact of becoming taxable

Once taxable, the operator collects 10% consumption tax on accommodation fees and remits the net amount after input tax credits. Tax paid on cleaning and supplies can be credited, but pricing mistakes may reduce effective yield. Eligibility for simplified taxation should also be reviewed in advance.

5. Takeaway

STR investing combines growth potential with consumption tax exposure. Monitor the ¥10,000,000 threshold and model after tax returns under both exempt and taxable scenarios. Clear tax classification makes STR performance easier to manage and forecast.