1. Basic Role of the Two Insurance Types

Minpaku operators must have both fire insurance and liability insurance.

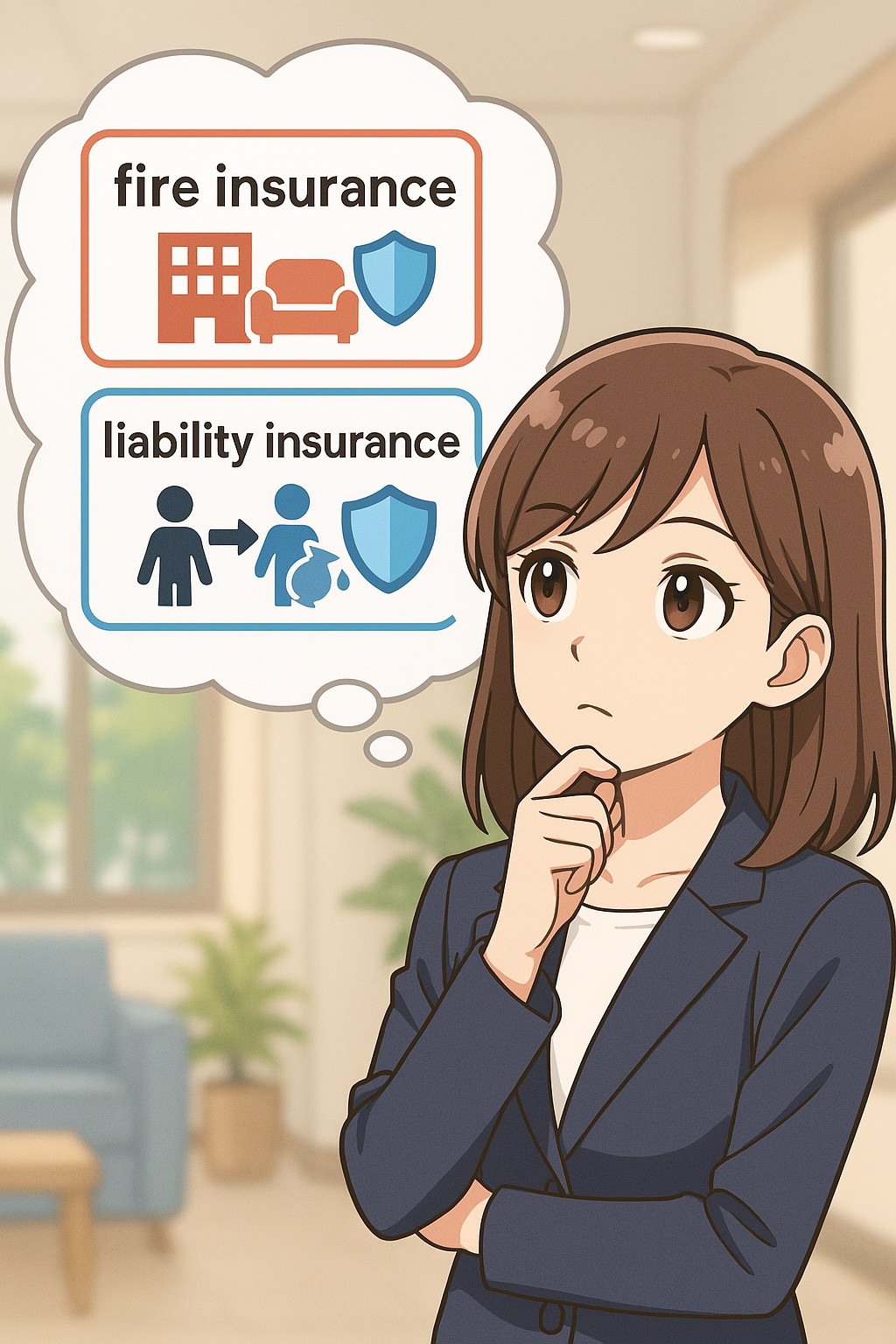

Fire insurance covers the building and furniture, while liability insurance covers damage to guests or third parties.

For registered lodgings under the Private Lodging Business Act, some municipalities effectively require liability insurance coverage.

2. Coverage Details and Selection Criteria

Standard fire insurance covers fire, lightning, explosion, wind, and flood damage, with optional add-ons such as water leakage, theft, and breakage.

Liability insurance typically applies when a guest damages equipment or causes water leakage that affects another unit.

A coverage limit of around JPY 100 million per incident is a practical benchmark.

When using a management company, confirm whether it is included under the insured party definition.

3. Case Study and Risk Control

For example, in Kyoto, a bathroom leak in a minpaku caused JPY 2 million in repairs to the downstairs unit.

Because the operator had liability insurance, there was no financial loss.

Without insurance, combined repair costs and lost revenue during downtime could exceed JPY 3 million.

Annual premiums are generally JPY 30,000–50,000, which is reasonable when annual revenue exceeds JPY 2 million.

Takeaway

For stable operations, always maintain both fire and liability insurance.

Verify coverage limits and conditions carefully to match your operation model. With proper protection, even unexpected accidents will not threaten the continuity of your business.